With the latest, and probably final, version of the Republican plan to repeal and replace Obamacare due to emerge Thursday, the party leadership is in the astonishing position of desperately trying to design a workable plan to meet their deadline. “I hate to break this one to you guys, but I don’t think they have any idea yet how they’re going to do this,” a senior Republican aide tells HuffPost.

As the deadline approaches, the endpoint of a coherent bill seems to be moving further out of reach. Senator Ted Cruz has been selling his colleagues on an amendment that would allow insurers to sell unregulated plans with minimal coverage, as long as they also sell regulated plans. That would split the market into two completely different risk pools, one cheap and healthy, and the other sick and expensive, an arrangement insurers call “unworkable.” Another Republican senator, Mike Rounds of South Dakota, is trying to undo the damage Cruz’s plan would do by creating some kind of “ratio” between the costs of the expensive insurance and the cheap insurance. Such an approach has never been tried, and no health-care experts have emerged to suggest it might work even in theory.

If you’re going to rush a secret plan into law, you really need to be working with an off-the-shelf policy. The health-care debate started eight years ago. Republicans have had a long time to whiteboard some ideas. They are trying to reconceptualize the problem almost from scratch over a few days. This is like the Airplane! flight attendant announcing, “By the way, is there anyone onboard who knows how to fly a plane?”

The attempt to hastily devise a fix for a problem the Republican bill itself creates is symptomatic of the degree to which their plan has lost all touch with its rationale. The putative reason Republicans have given for repealing and replacing Obamacare is that the law is a “train wreck,” “collapsing,” and so on. The individual health-care exchanges are supposedly heading into a “death spiral” of sicker customers, higher premiums, and fleeing insurers. GOP leaders have insisted they are on a “rescue mission.”

Even if the exchanges were collapsing into a death spiral, it would not justify their plans to slash Medicaid, a program that does not require actuarial balance and is not even theoretically susceptible to a death spiral. And in any case, a mounting body of evidence has found that the exchanges are stable. Financial analysts have said this, insurance actuaries have said it, even the federal government has said it.

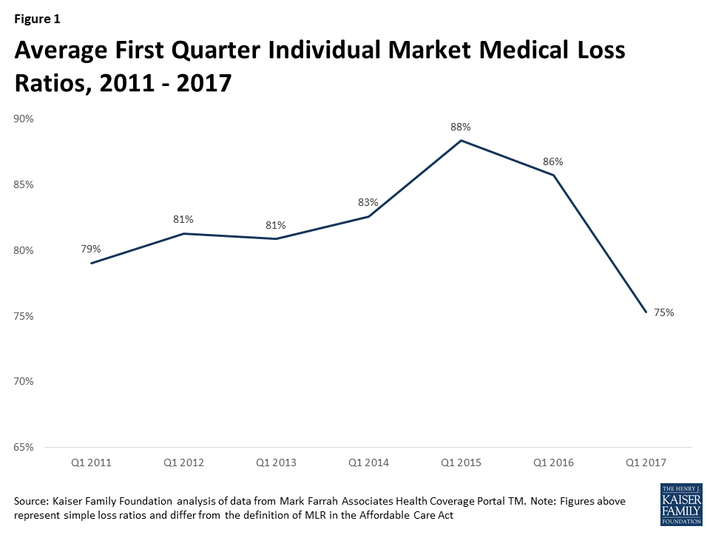

Recently, another piece of evidence has underscored the conclusion in even more detail. Cynthia Cox and Larry Levitt have a detailed report on the state of the markets. They conclude that insurers on the whole have found a stable price point. The “medical loss ratio,” which means the share of premium payments paid out in claims, dropped significantly in the beginning of this year:

Not surprisingly, insurers’ profit margin shot up:

Facing a brand-new market, insurers initially set their premiums far too low (and much lower than the Congressional Budget Office forecast). It has taken a few years, but they have corrected the error and settled in at a stable level. Republicans have cherry-picked horror stories of skyrocketing premiums, and it is true that 2017 saw premiums rise as part of this price correction. But there is zero reason to expect premiums to need to rise more.

Except, of course, for the fact that the government is run by people who are trying to kill Obamacare. Because of that fact, insurers in many states have fled the market due to political uncertainty. The Trump administration has followed a strategy of threatening to destroy the exchanges through sabotage, and then using the response by insurers to these threats as evidence that the law is collapsing on its own. Trump’s Department of Health and Human Services has put out press releases celebrating insurer exits from the marketplaces.

Health-care policy analyst Adrianna McIntyre noticed an interesting fact about these insurer departures. They are disproportionately concentrated in states where the exchange is run by the federal government rather than by the state. The National Academy for State Health Policy finds that state-based exchanges are not seeing their insurers flee the markets.

“With federally-facilitated exchanges that use healthcare.gov, the federal government is responsible for most exchange activities,” McIntyre tells me. “This includes consumer outreach, a function that is hugely important to insurers — if the Trump administration decides not to allocate resources toward outreach for the next enrollment period, insurers might reasonably expect that the people who do sign up will be sicker, on average.” If your business is dependent on cooperation from people who publicly celebrate every time a firm quits the market, you may have some reservations about staying in the market.

This policy makes perfect sense if your goal is to roll back the welfare state by any means necessary, or to undo as many Obama-era policies as you can. But that isn’t what Republicans have promised, and it isn’t what the public wants. (What the public wants, by nearly a three-to-one margin, is not to repeal and replace Obamacare but to work with Democrats and fix the law.) So the Republican Congress has to destroy a law that people like, and then replace it with something that replicates its current functions. They are scrambling to solve a problem that has no real answer.