The global economic recovery is running low on fuel. Chinese factories have been flickering on and off as Beijing rations electricity. Britons have been parking in petrol lines as their nation’s pumps run dry. Americans have turned on their president as spiking gas prices eat their wage gains. And the entire northern hemisphere is sweating the cost of keeping warm this winter.

High energy prices have long been the bane of the post-2020 recovery. But as the days grow shorter and the nights get colder, their salience is steadily rising. In recent days, Democrats and Republicans alike have called on Joe Biden to take immediate action to reduce the cost of energy. The former implored the president to bring down gas prices by tapping the nation’s emergency oil reserves. The latter chastised Biden for personally driving up energy prices by blocking new oil and gas drilling on federal land.

Meanwhile, fossil-fuel lobbyists and eco-socialists alike are casting the energy crunch as a byproduct of the world’s (slow and uneven) green transition. In their account, investors have been spurning new oil and gas production out of fear of future regulations, while renewables have failed to scale up fast enough to compensate. For oil barons, this narrative functions as an argument against stringent carbon pricing. For Marxists, it offers hope for an impending crisis of capitalism, as the old energy system dies and the new one struggles to be born.

Global energy markets contain multitudes. The price of oil internalizes myriad forces, from the financial to the macroeconomic to the geopolitical to the meteorological. So, one can tell a wide range of true stories about the energy crisis of 2021. But two of the most prominent narratives in American discourse — that climate policy is the primary driver of the global price spike, and that Biden could resolve the crisis if only environmentalists would let him — are simply false. Such myths do less to explain the present crisis of energy inflation than to undermine our prospects for rapid decarbonization. So it’s important to be clear about what they get wrong.

Why energy prices are high and rising.

The true origin of today’s energy crisis isn’t the 2020 COVID crash, but rather, the 2014 oil-price collapse.

In the first years of the last decade, China’s strong growth propelled a global commodities boom, and kept the price of oil hovering around $100 a barrel. This was a boon to energy investors in the short run. But the rally sowed the seeds of its own undoing. Forms of energy extraction that had been prohibitively expensive when oil was trading at $60 a barrel suddenly became eminently profitable. Capital poured into America’s shale industry. Thus, the supply of fossil fuel on global markets rapidly increased. At the same time, slowing global growth combined with advances in energy efficiency lowered global energy demand.

Traditionally, OPEC would have responded to such conditions by trying to stabilize global prices by pumping less oil. But Saudi Arabia saw opportunity in a sustained energy glut.

As a conventional oil producer, Saudi Aramco had a much lower break-even price than America’s shale drillers. And as a sovereign government with a foreign-currency reserve worth $750 billion, the Saudis could afford to sell energy at a loss for a lot longer than private firms in the Permian basin. Thus, by keeping the taps on and allowing global energy prices to crash, the House of Saud could reclaim the global market share that frackers had so rudely wrestled from it.

As a result, the price of oil plunged by 70 percent between mid-2014 and early 2016.

All this had two lasting consequences for global energy markets that are integral to today’s crisis. First, investors’ appetite for new oil and gas production collapsed. Global capital craves steady returns, not 70 percent price swings.

Long-term shareholders in fossil-fuel firms pressured managers to cut back investment in favor of dividends. Many such shareholders had sustained heavy losses during the crash, and therefore refused to sanction risky new projects until they recouped their initial investments.

Second, the combination of advances in fracking technology and a glutted energy market made natural gas unprecedentedly abundant and cost-competitive with coal. Utilities therefore started replacing coal-fired power plants with gas-fired ones, and the global electricity system became newly reliant on natural gas.

These changes in global energy markets lay the kindling for an energy crisis. COVID lit a match, and then bad weather rained down kerosene.

The COVID recession took a toll on both energy demand and supply. Thanks to unusually robust fiscal policy throughout the Global North, however, global appetite for energy rebounded much faster than supply chains did. This year has seen the highest pace of post-recession growth in eight decades. Yet 2020 also left behind a maintenance backlog in the world’s energy industry: Public-health regulations and outbreaks forced many producers to postpone upkeep operations that had been scheduled last year. This, combined with several unexpected outages and supply-chain dysfunctions, impaired the ramping up of production in 2021.

Adverse meteorological conditions exacerbated the mismatch between supply and demand. Last January brought extremely cold weather to much of Asia, causing a surge in the continent’s consumption of energy. Meanwhile, droughts in multiple regions reliant on hydropower, combined with below-average wind speeds in Northern Europe, yielded an unexpected reduction in the world’s renewable-energy capacity.

By themselves, these developments would have been sufficient to trigger a spike in energy prices. What’s kept prices elevated so durably, however, are the structural changes wrought by the 2014 oil-price plunge. Even before the COVID shock, energy production was failing to keep pace with rising demand. Alas, this year’s price jump hasn’t triggered any surge in “catch-up” investment within the oil and gas industry.

To the contrary, after years of poor returns, shareholders have forced fossil-fuel firms to prioritize windfall profits over new investment. This prioritization of dividends over drilling hasn’t just prevented private energy producers from raising production to meet soaring demand; it’s also stopped state-owned oil companies from doing so.

Like private investors in the energy sector, the OPEC nations and Russia suffered a prolonged period of disappointing returns after 2014. Now, they are eager to milk the current energy rally for all the revenue that it’s worth.

If U.S. shale drillers were responding to high prices by increasing production, then Russia and OPEC would have an incentive to respond to market demand; they remember what happened the last time that they allowed the price of a barrel of oil to approach triple digits, and do not want to lose market share to frackers.

But as Reuters reported last week, Saudi Arabia and Russia are now confident that “higher oil prices will not elicit a fast response from the U.S. shale industry.” As a result, they feel that they have more to gain than lose from letting prices continue to rise while they sit on their spare capacity.

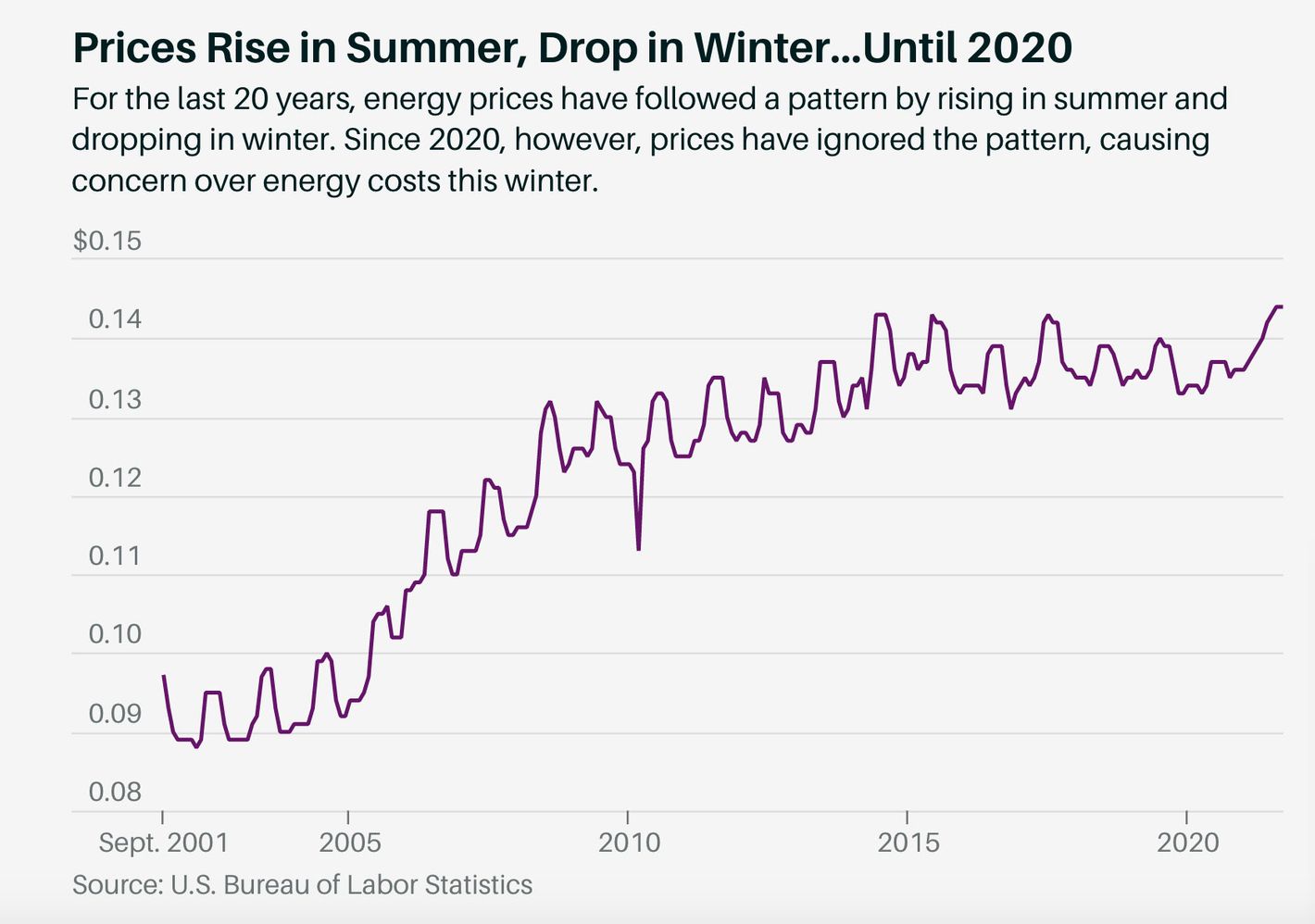

The second legacy of last decade’s energy glut and price collapse — the global advance of gas-fired power plants — has also proven problematic. It is far more common for people to heat their homes with natural gas than with coal. Thus, as gas has displaced coal on power grids, competition between the electric and home heat sectors for fuel in the wintertime has increased.

As Barron’s notes, U.S. electricity prices have historically tended to rise in the summer (as consumers turn on their air conditioners) and fall in the winter. But in 2020, this pattern reversed: As power plants bid against households for limited supplies of natural gas, electricity prices reached new heights in the year’s closing months.

This bodes poorly for the winter to come. The U.S. government expects home heating bills to rise by as much as 54 percent for Americans this winter relative to last year. And as households burn their disposable income to keep warm, they are also liable to see their electricity bills soar.

What’s climate policy got to do with it?

Last decade’s drop-off in oil and gas investment began just before the Paris Climate Agreement. Many observers have therefore been tempted to draw a causal arrow between the two: With decarbonization looming, fear of stranded assets chased capital out of the fossil-fuel sector, and public investment in renewables failed to fill the gap. Ergo, energy crisis.

This narrative is plausible on its face. And it isn’t necessarily untrue that concerns about climate policy have impacted new investment in fossil fuels at the margin. But it just isn’t the main story.

First of all, investment in oil and gas plunged after the 2014 price collapse, and stabilized in the years immediately following the 2015 Paris Agreement.

Second, as Adam Tooze notes, investment in pipelines for liquified natural gas (LNG) has been robust in recent years. LNG pipelines are long-term investments with significant upfront costs. They therefore are a poor financial proposition if one presumes that rapid decarbonization is nigh. Yet even Europe, where the price of carbon permits is set to steadily rise in the coming decades, is building out pipelines and LNG terminal capacities far in excess of its present needs. There is little sign that fear of an impending green transition is the primary force shaping investment in the energy sector.

Rather, as we’ve seen, today’s shortfalls in fossil-fuel investment and production derive from the geopolitical tensions and financial volatility that have long characterized the sector. Whatever the state of climate policy, investors in shale oil would want to recoup their 2014 losses this year, while OPEC and Russia would wish to press their present advantage. If we want a global energy system that is less vulnerable to the whims of Wall Street and petrostates, we need to accelerate the green transition, not back away from it.

This said, climate policy has been a secondary factor in this year’s energy inflation. The displacement of coal by natural gas in global electric grids was driven primarily by market prices. But emissions targets have also had an impact. The Chinese government has pursued a national policy of limiting coal power in favor of gas. And that transition has played a significant role in Europe’s energy troubles. Reliant on gas imports from Asia, Europe was ill-prepared for heightened competition from China over the region’s limited gas supplies.

In an earlier era, rising gas prices might have led Europe to pivot toward coal. But the rising cost of the E.U.’s carbon permits rendered this economically nonviable.

So green policy has elevated global demand for natural gas. But it has relatively little to do with the present constraints on supply.

Joe Biden alone can’t fix it.

In recent weeks, the president has implored Russia and OPEC “to pump more oil,” while maintaining his opposition to new oil and gas drilling on lands owned by the U.S. government, and rhetorical support for a swift green transition.

Republican senators have taken umbrage at this conduct, informing Biden in an August letter, “It is astonishing that your administration is now seeking assistance from an international oil cartel when America has sufficient domestic supply and reserves to increase output, which would reduce gasoline prices.”

Certainly, there is an irony in the president of a major oil- and gas-producing nation begging foreign governments to produce more oil and gas. Still, the GOP’s criticism is mostly hot air.

Unlike their counterparts in Russia and Saudi Arabia, American energy producers are not just sitting on tons of spare capacity. OPEC has the resources at its disposal to rapidly increase the global energy supply. U.S. firms don’t. Rather, they’d need to drill and complete new wells to comparably increase oil and gas volumes, a process that would take months. More fundamentally, the American energy industry sits in private hands. Joe Biden does not have the authority to order an increase in oil and gas drilling, and Republican senators would surely impeach him if he tried to impinge on the private sector’s prerogatives in that fashion.

Meanwhile, Biden’s curb on new drilling on federal lands is doing precisely nothing to limit production. As already emphasized, oil and gas investors simply are not interested in expanding production. And even if they were, U.S. companies already own drilling rights on “so much federal acreage that they have enough to drill for years without needing to apply for more permits,” according to Barron’s.

Biden could tap America’s Strategic Petroleum Reserve. But analysts say this would only deliver a small, temporary reduction in oil prices. More radical measures, such as a ban on oil and gas exports, would likely backfire. If America cut off the world’s access to its domestic energy supply, global oil prices would rise. And since American oil refiners are dependent on foreign oil supplies to make gasoline, higher global oil prices would yield higher U.S. gas prices.

With Congress’s help, there are things the president can do to ease pain for low-income consumers, such as increase federal funding for home-energy assistance. But Democrats can’t do very much to ease supply constraints in the near term.

What they can do is render America’s energy system less vulnerable to outrageous commodity cycles in the long term by increasing investment in renewable energy. Let’s hope mythic misconceptions about today’s energy inflation don’t stop them.