Not since the British government imposed the Gregorian calendar on the American colonies in 1752 has there been such scheduling havoc in New York. As people debate how best to commemorate September 11, others are worrying about how to plan around the mournful anniversary: The usual post–Labor Day social-season kickoff – charity galas, book parties, movie premieres, fashion events – has been postponed while publicists and social committees wrestle with questions of taste and timing.

One public-relations exec says she recently persuaded a foreign client to delay the opening of a new Manhattan boutique until later in the fall. “How shallow can you be to try to hype $600 blouses in September?” With Fashion Week pushed back to start the 18th, planners are scrambling for acceptable dates for pre- and post-collection celebrations. “I wouldn’t touch the week of September 11,” says publicist Nadine Johnson. “And nobody wants to do anything on the 18th or 19th either.”

The same nervous mood extends to the book circuit. “Normally, the season for authors commences the day after Labor Day, but this year it will start September 16,” says Random House spokesman Stuart Applebaum. Given that TV shows and newspapers will be saturated with remembrances, he says, trying to plug a new novel would be inappropriate (and unprofitable).

At entertainment networks, programmers are also concerned about striking the right tone. “We want to be respectful,” says Patty Newburger, Comedy Central’s vice-president for films, who has pushed back the air date for the network’s first original movie, Porn n’ Chicken, a true-life tale of Yale students who went from watching porn to (pretending to) make it. By mid-October, however, she thinks viewers will welcome a comic romp.

Just how long the social blackout should last is being quietly discussed all over town. Society caterer Sean Driscoll, co-owner of Glorious Food, says that the 11th, combined with the early Jewish holidays, means the caviar-canapé circuit will be slow mid-month: “We don’t have anything yet for September 11, 12, 13, 14, 15, or 16.” Adds Liz Neumark, owner of the caterer Great Performances, “I’ve never seen such fear and uncertainty. Everybody’s afraid to be the first to book.”

Of course, there are those contrarians who expect New Yorkers to fall silent for a day or two and then carry on. As movie publicist Peggy Siegal says, “I can’t see the entire city coming to a screeching halt in September.” Restaurateurs and hoteliers hope she’s right. Drew Nieporent, who is considering closing Montrachet and Tribeca Grill on the 11th, says, “I think it’ll be a one-day issue. If we keep mourning this, we’ll never get over it.”

And then there are those unfortunate organizations that find themselves locked into September dates arranged years ago. Paul Kellogg, the general director of the New York City Opera, sounds somewhat pained as he explains that he can’t reschedule the September 10 gala opening since the opera shares the Lincoln Center hall with the ballet: “We have very little flexibility,” he sighs. Last year’s gala, on September 11, was canceled, and this year’s scaled-down version offers only a dinner before the performance for the $500-a-ticket patrons and no dancing afterward. “It’s totally inappropriate to do a celebratory party,” Kellogg says, “but we hope people will find solace in the music.”

Who doesn’t have a fraught relationship to money? What makes money problems a “disorder”? Debtors Anonymous’s poignantly titled Friday-night “Prosperity Meeting” puts the question to rest. It is filled with people who are drawn to “getting to zero,” literally as well as figuratively (“When I see a couple of hundred dollars in the bank, I have to spend it”). They grope for metaphors of breath to explain how vital their money problems feel: They are drowning or crushed or pressed or flattened by mountains of debt. They do things like freeze their credit cards into blocks of ice and then go ahead and call Lands’ End and use the number anyway. “It’s as if I keep my dollar bills on top of my head and whenever I step out, they just blow away,” a man complains. An Upper East Sider reflects how she married three times for money – three! – in order to underwrite compulsive spending before she got help.

Although money has always been an important motif in psychotherapy, thinking about how to treat money problems has begun to change in recent years. Such problems had always been considered secondary symptoms of neurotic conflicts or underlying mental illnesses, such as bipolar disease. However, clinicians have observed that money pathology, like alcoholism, has a tendency to take on a life of its own, and become a dominant defining condition. The DSM (the Diagnostic and Statistical Manual of Mental Disorders) may include “compulsive shopping” in its next edition, in a section on impulse-control disorders, such as compulsive gambling and kleptomania. Such an inclusion would make it an official, insurance-covered psychiatric disorder.

Carl Jung defined addiction as a low-level spiritual quest – a phrase that seems to capture the truth that the longings that drive addiction also drive the basic human quests for love, meaning, and peace. The snake in the garden of addiction is the transience of its fruits. The addict’s pathology is underscored by her keen awareness that her satisfactions are increasingly brief and her letdowns increasingly cruel – and by her decision to keep at it anyway.

Overspending generally divides along gender lines: 70 to 75 percent of compulsive gamblers are male, whereas 80 to 90 percent of compulsive shoppers are female. According to Harvey Greenberg, professor of psychiatry at Albert Einstein College of Medicine, existent studies suggest compulsive shopping affects between 1 and 5 percent of the population (in comparison, anorexia and bulimia affect almost 3 percent.) Compulsive shoppers average $20,000 to $27,000 in credit-card debt. They gravitate toward crowded stores, buzzing with action and lit timelessly, like casinos, where they experience rising tension and excitement. But they also describe a sense of agony, of wrestling to control their impulses even while succumbing to them. At the moment of purchase, they feel a sense of relief, satisfying as an orgasm, followed by depressive deflation, despair, and guilt. Interestingly, studies show the same letdown among rich and poor women alike, suggesting that the depressive effect is not a result of regret over having spent money they can’t afford but an organic part of the cycle.

“There’s a rush of anxiety at a sale – it’s a kind of high,” A.J. says. “It’s a very primal thing, the hunt of it – riffling through clothes, competing, scoring: spearing something with your credit card.”

Yet the shopper typically has little interest in the things themselves. One sign separating a compulsive spender from an ordinary shop-till-you-drop type is the tags still hanging on her walls of clothes. Sarah Jessica Parker may have hundreds of pairs of shoes, but she actually likes shoes, whereas one of Ron’s clients, who has 300 pairs, wears the same shabby loafers day after day.

Although society tends to diagnose such people as suffering from terminal shallowness, compulsive shopping behaves similarly to – and is often accompanied by – other disorders, such as anxiety or depression. Treatment may include Prozac and mood stabilizers such as lithium. Although it typically begins in adolescence and blooms in the late twenties and early thirties, its causes remain obscure. In psychoanalysis, it is viewed as a complex symbolic restitution redressing low self-esteem, fear of death, depressive emptiness, and the filling of a void.

Since – unlike the Debtors Anonymous crowd – none of Ron’s clients is actually poor, it’s easy to see that the source of their problems is in their heads, not their wallets. (His fee selects an affluent population: $150 for a 45-minute session, with a typical spending plan requiring at least eight sessions for setup and many more for maintenance.) But in contrast to traditional therapy, Ron’s counseling does not focus on plumbing the patient’s emotions. “The hope that insight-oriented therapy will translate into behavioral changes doesn’t work with money addictions any more than it did with alcoholism,” he says. “First, you have to stop the behavior.”

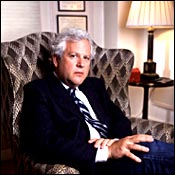

Ron’s authority, like that of most addiction counselors, is based as much as anything on personal experience. At 49, he has a prosperous, well-fed look, with silver hair, baby-blue eyes, and little round reading glasses he puts on when looking at figures. His rapid-fire questioning style betrays the manic businessman he once was.

“I have dollar signs in the synapses of my brain,” he is fond of saying. His lineage includes a Cain-and-Abel fable: His uncle, Herb Gallen (the founder of the clothing line Ellen Tracy), was rich; his father, who worked for him yet didn’t speak to him, “was not.” Ron inherited his father’s money lust. He recalls walking down Fifth Avenue one day while calculating the cost of the clothing he was wearing, which included a Bijan suit, “to see if I was okay – if the figure was high enough,” he says. The sum was a satisfying $10,000. Should he add his Rolex watch, he wondered?

Drinking, scoring cocaine, and trying to retain the attention of a high-maintenance model, he woke up in the summer of 1987 seven figures in debt, with calls from 48 creditors. He went into recovery and eventually became an alcohol-and-drug counselor. But he came to feel that the missing piece of his clients’ treatment was money.

In his recently published first book, The Money Trap, Ron describes many versions of the disorder: money obsessives, overspenders, and underearners, or what Debtors Anonymous terms “anorectic spenders.” The latter group are afraid of spending – and often of earning – money, like the client who is proud that he has brought the cost of his breakfast down to 9 cents a day by buying oatmeal in bulk. People frequently suffer from a confusing combination of underspending and overspending: The oatmeal eater has a $160 million portfolio and favors Italian suits. Another equally wealthy executive earnestly explained to Ron that he had started ordering tap water at lunch because he couldn’t afford Perrier. A woman client spends $4,000 a month on clothes but hasn’t bought underwear in three years.

Most overspenders have a primal moment of deprivation – a time they couldn’t afford something they really wanted and couldn’t tolerate the feeling that provoked. The anorectic spenders respond in the converse way; they deal with not being able to afford something by shutting down their desires. Living like church mice makes them feel safe. “Anorectic spenders are seeking the same sense of control as anorexics,” Ron says. “But when you start shrinking desire, you always overshoot the mark.”

The pitch that Ron makes to his clients is that a spending plan is totally different from a budget. “A budget is about what you can’t do,” he commences. “A spending plan says: I have all this money and I get to spend it however I want. Budgets fail for the same reason diets fail. We rebel against internalized parents as much as real ones.” The success of his treatment may hinge on whether his clients buy the distinction.

Developing a spending plan begins with a trip to “the Everything in the World Store – the store where there is food, housing, trips to the Caribbean, CDs, and cashmere.” After taking out money for taxes and agency commission, A.J. has $6,632 a month to bring to that store. From that, $487 is designated for debt repayment and $560 for savings – 8 percent of take-home pay, which will cover one month’s expenses in a year’s time. Ron recommends that self-employed people keep a six-month reserve. Since an overspender’s dominant fear is deprivation, self-care is always the first category in his or her spending plan. “Self-care is a different thing for everyone,” Ron says. “What we want to find out is, what does it mean to take care of A.J.?”

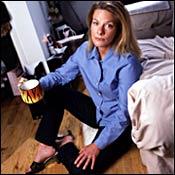

By junior high school, studies have shown, kids have sophisticated methods for reading visual clues about economic status. The messages that A.J.’s appearance conveys, however, are confusing. “A funny mixture of expensive and cheap,” Ron – who used to work in the clothing industry – tells me.

The money part of the message today is a silky Pucci-inspired magenta-and-lavender shirt, a short black leather skirt, and shiny black leather high-heeled boots. But squarely in front of the couch is a sad Canal Street imitation of a Louis Vuitton bag. And her hair is an unnatural shade of gold – a color she obtains through using the old-fashioned peroxide bleach Sun-In because “coloring is so expensive.”

“What clothes do you need to take care of you over a year? I’m not asking what clothes you want or usually buy,” he reminds her, “but what do you truly need?”

What’s striking about A.J.’s reply is less the prices than the volume. It’s as if she’s picturing shopping for a naked orphan rather than for a woman whose closets are groaning. Her words trip over each other as she lists four skirts a year (two $100 skirts, one $20 skirt, and one $200 skirt), three to four $50 pairs of jeans, two $500 evening dresses, four $150 jackets, one $200 coat, five $50 sweaters, fourteen $50 tops, ten $100 pairs of shoes (five for winter and five for summer), two $200 pairs of boots, two $75-to-$100 pairs of sneakers, one really nice $500 handbag, two $50 ones, and one $20 Chinatown knockoff. Although she doesn’t indulge in real jewelry, she says, she buys $100 worth of costume jewelry each month and five $100 bottles of perfume a year. Punching underwear, gloves, scarves, hats, nightgowns, and a warm-up suit into his calculator, Ron brings the total to $8,556 a year – or about 10 percent of her take-home pay.

“When we add that to your other expenses, you’ve already overspent your income, even without paying back your debts or saving,” Ron says.

Ron asks if she has other addictive tendencies, and she says she has always struggled with her weight and with eating sweets (though there’s no visual evidence of it). She nods when he asks, “Is sugar a trigger for you to shop? If you eat a frosted cake, do you feel you might as well buy a twinset because you’re already in free fall?”

He moves to the trickiest area: giving money to Tony. In Ron’s program, giving money is practically as taboo as borrowing money – it’s sharing your stash, it’s co-dependency, it’s bad for you and bad for your dependent. He fires a series of questions at her designed to ferret out why Tony can’t live on his $50,000 salary (“Booze? Grass?”). A.J. seems extremely offended. She doesn’t know what Tony spends money on, but she thinks he wouldn’t ask if he didn’t need it, and she doesn’t want to say no: “He’s supported me in the past. I can’t lecture him about money.”

“If you can’t put a boundary around that, then you can’t have a spending plan,” Ron says.

None of the plan Ron designs with A.J. over the next five sessions seems to require undue sacrifice. Instead of planning an $8,000 wardrobe, could she budget for a $5,000 one? “By giving yourself permission to shop, you’ll break the taboo that drives the compulsion,” Ron assures her. Some of the savings will be transferred to new categories of self-care, to try to cultivate pleasures besides shopping: She’ll go to the opera once a month, take a cooking or language class, save for a trip to Italy, and get a housekeeper – all things she had thought she couldn’t afford.

But will she follow the plan?

“Most addiction programs have a success rate of 25 to 30 percent,” Ron tells me. “I have an astonishing track record of 50 percent.”

“Ron talks a good talk,” A.J. says. “But I don’t know if I can put my money where his mouth is.”

In her book The Overspent American, Harvard economist Juliet Schor describes what she calls the “new consumerism”: the way in which the culture of spending has changed and intensified in the past half-century. In the early postwar decades, Americans spent to keep up with the famous Joneses – to not be the last one on the block to have a car or automated washing machine. But now the ethos has changed from spending in order to conform to spending in order to express individuality – a much more expensive proposition.

Moreover, everyone in the Joneses’ neighborhood earned roughly the same amount, so keeping up with them wasn’t too much of a stretch. Today, however, our “reference groups” are much more diverse and include co-workers or TV “friends.” Yet, Schor writes, when “poet-waiters earning $18,000 a year, teachers earning $30,000, and editors and publishers earning six-figure incomes all aspire to be part of one urban literary referent group, which exerts pressure to drink the same brand of bottled water and wine, wear the same urban literary clothing, and appoint their apartment with the same urban literary furnishings, those at the lower end of the spectrum find themselves in an untenable situation.”

The result is that only one third of households making more than $100,000 a year (and 40 percent making $50,000 to $100,000) agree with the statement “I can afford to buy everything I really need.” Overall, “half the population of the richest country in the world say they cannot afford everything they really need,” she concludes. “And it’s not just the poorer half.”

Nowhere are these problems more evident than in New York – a city in which there is no middle class, or where middle-class life requires upper-class means. Lisa O’Brien, president of the New York Charter Schools Association, is typical of the six- and seven-figure hand-to-mouth earners: She and her husband, Daniel, a commercial-real-estate developer, still have trouble paying off their American Express card some months even though, after some bad business years, Daniel’s income topped $1 million last year. Although they’ve finally succeeded in taking care of the balance of their $100,000 Saratoga Springs wedding five years ago, Daniel only opened a 401(k) last year. “It’s unbelievable,” she says, her perky voice dropping. “How can we make so much and have this little to show? I wasn’t raised to live like this. It’s a sickness.”

Most Americans rely on credit cards to fill the gap between reality and desire. Many spending disorders would remain latent tendencies without the enabling credit cards. Kim Miller, for example, who spent $60,000 on consumer goods while getting a Ph.D. in English at suny–Buffalo, had 21 credit cards: Whenever she maxed one out, there was always a fresh start greeting her in the mail.

According to economic sociologist Robert Manning, author of Credit Card Nation: The Consequence of America’s Addiction to Debt, 60 percent of Americans do not pay off their balance in full each month; these families average more than $12,000 in credit-card debt, which means they’re paying $1,800 to $2,200 in interest alone every year. And at 18 percent, interest rates have never been farther from the prime-lending rate, 4.75 percent. (Many of the people carrying balances would be eligible for bank loans against their mortgages.) Paying the minimum monthly balance on $12,000, it would take at least 30 years to reduce the debt.

The average rate of savings fell from 10 percent of income in 1980 to zero in 2000 – a fact that economists fear will have long-term negative consequences for the economy as a whole (although savings increased very slightly as consumption has declined during the recession). People are offered credit lines that are much greater than they can afford with their income. If applicants dissemble a little on the form, the disparity can be increased exponentially. Yet attempts at credit-card reform are routinely defeated. (The credit-card industry was a major campaign contributor to President Bush.) The result: One in 69 American households has filed for personal bankruptcy. And the figures are likely to go up.

Like other people with money disorders, A.J. has plenty of insight into her problems’ origins, but – as the saying goes – the insight never put a nickel in her pocket. “On a good day – a non-bloating, going-to-the-gym day – shopping is a celebration,” A.J. explains matter-of factly. “On a bad day, it’s making up for feeling fat and ugly and hairy like a monster.”

In North Carolina, her family lived near the poverty line in a preppy, class-conscious area – the kind of place where all the kids wore Polo Ralph Lauren and the like. All of her feelings of insecurity became transposed onto these external differences – feelings with which her parents did not empathize. She sees her “propensity for label-whoredom” now as all about trying to “go back and get acceptance from the peers who rejected me as a small person who didn’t have the right uniform.” She remembers once as a child cutting out a paper alligator and pasting it on a Dollar-Mart shirt. It still pains her to think about how it didn’t fool anybody.

Her first attempt at getting help was five years ago when she went to BuCCS, a debt-consolidation agency. Debt-consolidation agencies were originally a noble idea, funded by the banks, but as their numbers grew they were underwritten by credit-card companies themselves. The credit-card companies pay the agencies a kickback – a percentage of the debt they were able to collect from clients – creating an inherent conflict of interest. Under the guise of nonprofit organizations, the agencies, in fact, function as collection agencies of last resort (their boards are often dominated by people who work directly for credit-card companies). Although BuCCS is one of the better agencies, A.J. wasn’t able to adhere to the plan it created for her because the psychological problems that got her into debt had not been addressed.

“Like personal bankruptcy, debt-consolidation agencies are Band-Aid solutions to addiction,” Ron says. “They call themselves counseling bureaus, but they don’t really offer any. People immediately get new cards, and a year or two later, they’re in more debt than ever.”

The next time A.J. comes in, she’s been promoted to the position of “breakdown writer” (someone who generates plots rather than dialogue) with a raise in salary – a turn of fortune Ron sees as “potentially dangerous for someone trying to stabilize on a plan.” A boost in salary can temporarily hide a spending disorder and thus actually feed it.

Indeed, backsliding is in evidence today. A.J. has celebrated the news in her usual fashion, and plops down in front of her several big bags of celebration. When she holds up a silver-tipped chocolate faux-fur coat from Benetton, I exclaim, “Oh, that’s a deal!” and Ron glares at me. One of the spending-plan rules is never to buy on sale. “If it’s on sale, you tell them you want to pay full price. You are through buying things to ‘save’ money,” he says. (I know sales create a unique mind-set. My friend Amanda and I have a system we call Princess Math, based on the principle that a penny saved is a penny earned. We calculate our sale “earnings” and leverage them into more sale clothes!)

A.J. says that while she was shopping, she reassured herself that Ron would take away her privileges during the next session, which, of course, made her want to buy everything she wanted now (if you can’t follow the plan in a given category, the category is eliminated for a few months).

But Ron declines to rescind her privileges. “In your case, it would only trigger a major binge,” he says.

Behind the expenses people own up to are always the expenses they don’t own up to. On her sixth session, A.J. reveals a small detail: She has to pay for her upcoming wedding. Weddings can drive any bride crazy, but for a compulsive spender, they’re like New Year’s Eve for an alcoholic. When Ron takes out his calculator and she gives the estimates, the 100-person event comes to $33,500 – “at least” ($5,000 for rental of Landmark on the Park, an event space on Central Park West, $10,000 for the caterer, $4,000 for flowers, $5,000 for the band, $3,000 to $5,000 for the photographer, $1,000 for a Vera Wang sample-sale bridal dress, $1,000 for hair and makeup, $2,500 for liquor). Eleven thousand dollars has already been put down in deposits, which leaves $22,500 to pay and only three months in which to save it. Her parents will contribute, and she hopes her fiancé will, too.

“But he can’t even live on what he earns,” Ron snorts.

“But he could if he spent it more carefully,” A.J. says.

“What makes you think he’s going to change?”

A silence falls on the room. A further silence ensues when Ron presses the issue of what will happen when she doesn’t have money in her account to pay on the wedding day. She says she asked her guests to give cash in lieu of presents. But, Ron points out, if every couple gives $150, the total would still come to only $7,500. “You want to come home from Venezuela to a slew of angry calls from vendors?”

The crossroads is suddenly clear. Would she rather be the Princess Bride of the hour, surrounded by illusions of riches, or take the first step toward forging a new, solvent family?

“You want your checks to bounce?” Ron juts his head forward, his dramatic, inflected voice fills the room. “Blecch!” he says. “Blecch!”

A.J. flinches. It’s clear he’s lost her, as she tears up. “I just want to be a beautiful bride,” she says.

Yet the conversation haunts her. Once the financial details of her wedding have been brought to consciousness, they feel like an elephant trampling her dreams. “Every element of fun and joy has been turned into dollars and cents in my head,” she says.

A few weeks later, A.J. is given notice at her job. Though she knows it’s a fickle business, she’s still crushed. “I feel so defrocked,” she says. She has $1,500 in the bank and all the old debt. Shecancels her sessions with Ron and her plans to go into psychotherapy on the grounds that she can no longer afford them. She goes to the 50 percent discount rack at the drugstore to buy cheap shampoo. But she decides to go ahead with the $30,000 wedding. When the turnstile at the subway one day rejects her MetroCard, she has a flashback: Has Discover somehow found her again? Then she realizes the card is simply bent.

Her birthday fell in her final week of work. As an adopted child, she has always felt sensitive about it because she pictures her birth as an unhappy event. She decided to go with Tony to Da Silvano, the downtown Italian restaurant, and bought a $160 dress at “the crack house across the street,” the department store Century 21. She told Tony – whose company is going under – that she would pay for dinner. But as soon as they sat down, she realized she wanted him to pay. Her stomach began to hurt. She doesn’t remember the vintage of wine they ordered, only that it cost $89. When the tab came, she felt sick. It was $300: one quarter of her remaining assets. Could she discern a fine bottle of wine in a blind taste test?

“It wasn’t blind,” she says without irony. It had a familiar taste – one that satisfied an old craving. It tasted expensive.

“She hasn’t reached bottom,” Ron comments philosophically. “When she’s bottomed out, getting better – not having a fancy wedding or buying a new outfit – will be her top priority. But these kind of deep problems don’t develop overnight, and they don’t disappear in a matter of months! Some people get better before they get worse; some bump along the bottom for a long time.”

He says he hopes he’ll hear from A.J. again. “I think she’ll get better. I certainly hope so. But,” he adds, the customary certainty of his tone receding slightly, “the truth is, in any kind of addiction counseling, we never know who is going to get better – if I were to say at the beginning of this process, I’d be wrong as often as I’d be right.”

Also: Ten Steps To Take If You Think You Have a Money Disorder