Yesterday was Volcker Rule Day on Wall Street – the long-anticipated day when the rule reining in risky trading at big Wall Street banks was released, and a phalanx of $800-an-hour lawyers descended on the 71-page document with the tenacity of a pit viper, trying to figure out what it all meant for their big-bank clients and, more important, looking for loopholes.

The lawyers haven’t come up for air yet, but the bloggers have, and they’re fighting about whether or not the final Volcker rule actually works. The FT editorial board says, “Nuh-uh,” Tyler Cowen says, “No, not really,” former Senator Ted Kaufman says, “Hell, no,” Mike Konczal says, “Yes, mostly,” Matt Levine says, “Sure, why not?”

But the debate about whether or not the Volcker Rule – which has come to symbolize the entire Dodd-Frank Act, and serve as a proxy for its relative toughness on Wall Street – will work is mostly moot. Because in most of the ways that it could have possibly done so, the Volcker Rule already has worked.

Let’s take a trip back in time. In 2010, when the Volcker Rule was born, Goldman Sachs had an entire unit, Goldman Sachs Principal Strategies, designed for prop trading – essentially, betting the firm’s own money on stuff. It was closed, and most of its people moved to a private-equity firm. Morgan Stanley had a prop-trading unit with 60 employees. It got closed, too. So did the prop-trading divisions at Bank of America and Citigroup.

The Volcker Rule pushed all of those units out of banks, and most of their employees ended up in hedge funds and private-equity firms. That’s exactly what was supposed to happen – a transfer of risk away from too-big-to-fail, FDIC-backed banks to parts of the industry that could absorb losses more cleanly.

There is still risk inside banks, of course, and Volcker is supposed to address that, too. Under the new rule, banks aren’t supposed to take stuff onto their own books unless they plan to keep the stuff for more than 60 days, unless there is “historical customer demand” for the stuff among the bank’s clients (meaning that the bank is reasonably sure it can sell the stuff to someone else, soonish), or unless the stuff is designed to “hedge” other risk, making the bank’s overall portfolio less risky. (For more details, you can read the full text of the rule here.)

Let’s look at just that last bit – the hedging – since it’s at the heart of most people’s worries about how the Volcker Rule will look in practice. According to the Times, Treasury Secretary Jack Lew’s litmus test for the rule was whether it would have prevented the London Whale trading mishap at JPMorgan Chase, when a trader in the bank’s chief investment office amassed a huge credit position by tweaking a few Excel models to make the associated risk look smaller, and then lost $6 billion when he got trapped in the trade.

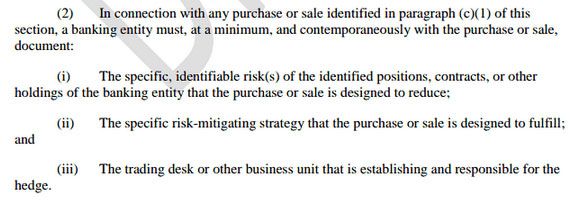

The Volcker Rule probably wouldn’t have stopped JPMorgan from classifying the Whale’s bet as a hedge. It was a hedge, albeit an extraordinarily poorly designed one. But the rule would have made it impossible for the hedge to have gone unmanaged for so long. Here, for example, is what a bank has to do if it wants to make a “risk-mitigating hedge” under the Volcker Rule:

Basically, the bank has to write down what the hedge is, why it’s needed to offset risk elsewhere in the portfolio, and why it shouldn’t be classified as a prop trade. For Bruno Iksil to sell massive amounts of protection on CDX IG.9, he would have had to write up the trade, label its specific function and amount, and pass it off to the firm’s lawyers and compliance officers, who would have seen how crazy it was and nixed the trade before it blew up. In other words, a Volcker Rule would have given the London Whale a few more handlers – and it’s that added supervision that matters, not the specifications of the rule itself.

Levine gets at this concept well:

Sure a lot of the Volcker rule is highly over-engineered checklists and admonitions that boil down to “don’t be dumb,” and sure there are good theoretical arguments against that sort of regulation, but I don’t know, come on. You shouldn’t be dumb. You could do a lot worse than a rule that requires you to think about what you’re doing.

The goal of the Volcker Rule was never to eliminate risky trading altogether. It was to eliminate the most blatant types of prop trading, and make it easier to examine the other types of trading for evidence of prop-ness. That’s more or less what the Volcker Rule will do. If Goldman Sachs wants to keep doing what is obviously market-making trading (lining up buyers and sellers of assets, an activity permitted under Volcker), it won’t have a hard time doing so. And if Goldman wants to wander into the gray area between prop-trading and market-making (buying assets, holding them until a seller can be found, and pocketing any price appreciation in the meantime), it will just have to justify why it did the trade that way.

Making sure those justifications are sound, and not just end-runs around the Volcker Rule, will be the job of future regulators, and it’s an important one. But the Volcker Rule was never meant to decide those case-by-case judgments. It’s just the mechanism that forces big-bank traders to enter the decision matrix.

Moreover, Wall Street has been operating under Volcker-like rules since 2011, when a draft of the rule circulated and banks began realigning themselves accordingly. Firms that lived and died by their prop-trading desks are now flourishing as safe, boring brokerages. Goldman Sachs and other firms that still operate big trading desks are finding those desks much less profitable. And bank traders who used to gamble in search of big bonuses long ago left for hedge fund and private-equity firms, where they don’t have compliance officers looking over their every move.

These were all expected results of the Volcker Rule, and the fact that the draft rule managed to escape the lobbying process more or less intact is actually pretty incredible. So while Volcker Rule supporters can hope for tough enforcement in the future, they should be happy with what’s already happened. After all, today’s Wall Street is very different – and better – than it was just a few years ago.